Last update: 06.11.2025

Poland has emerged as one of Europe’s most attractive investment destinations, offering a stable economy, dynamic growth, and business-friendly regulatory environment. Poland was among the first countries in the region to establish SEZs (special economic zones) as part of its strategy to attract investment and promote economic development.

For foreign investors seeking strategic market access, cost efficiency, and innovation potential, Poland presents numerous advantageous instruments and incentives designed to stimulate business expansion and maximize returns.

In addition to these measures, Poland offers a range of fiscal incentives, including tax exemptions and deductions, to further support business growth and regional development. You will find bellow the key tax instruments which are often applied.

PSI – Polska Strefa Inwestycji for economic growth

What is PSI?

The Polish Investment Zone (PSI) is a nationwide support scheme for new investments in Poland. Under PSI, investors can receive income tax exemptions (including CIT) based on a decision issued by the relevant authority.

Key benefits for investors:

- Corporate or personal income tax exemption for up to 15 years,

- The ability to invest anywhere in Poland – urban or rural,

- A simplified and fast-track application process,

- Institutional support during the investment process.

Who is eligible?

- Micro, small, medium, and large enterprises,

- Investors planning new tangible asset investments (e.g., construction of a new facility, purchase of machinery) or expansion of an existing business,

- Companies from various sectors – except for certain excluded activities such as retail, wholesale, alcohol and tobacco production, and several others.

- Please note that legal amendments are on their last stage and production of weapons, ammunition and explosives will also be eligible for PSI tax exemption.

Conditions of PSI:

- The minimum investment value depends on the company’s size and the location (lowest thresholds apply to SMEs in high-unemployment areas),

- The investment must align with regional development goals,

- Investors must meet qualitative criteria for social and economic sustainability

R&D relief Under Tax Incentives

What is the R&D Tax Relief?

The Research and Development (R&D) tax relief is a fiscal incentive that allows companies to deduct additional eligible expenses related to innovation and development projects from their taxable income. It encourages businesses to invest in new products, services, and processes – regardless of the industry.

Key Benefits for Businesses:

- Additional deduction of up to 200% of eligible R&D costs,

- Lower taxable income, resulting in a lower corporate or personal income tax bill,

- Applicable even if the company is not profitable – unused relief can be carried forward,

- No need to be a certified research institution – the company just needs to carry out qualifying R&D activities.

Who is eligible?

- Any business entity subject to CIT or PIT – including sole traders, partnerships, and corporations,

- Companies of all sizes and industries,

- Firms engaged in actual R&D work, even on a small scale.

Basic Conditions

- Incurred eligible (qualified) R&D costs, including:

- Salaries of employees involved in R&D activities,

- Purchase of materials or components used in R&D,

- Depreciation of machinery, equipment, or labs used in R&D,

- Fees for external expertise, technical opinions, or consulting services,

- Accounting records must clearly separate and document these expenses,

- The R&D work must be systematic, creative, and aimed at developing new knowledge or solutions.

Attracting foreign direct investment with other reliefs in Poland

Expansion relief (Tax Deduction for Increasing Product Sales)

What is it?

This relief allows companies to deduct additional costs incurred to increase revenue from product sales, such as entering new markets or acquiring new customers.

Key Benefits for Businesses:

- Up to 100% additional deduction of qualified “expansion-related” expenses (e.g., marketing campaigns, trade fairs, promotional materials, tender documentation).

Who is eligible?

- Businesses that sell their own manufactured products, regardless of industry or size.

Basic Conditions

- Expenses must be aimed at increasing product sales (not services),

- The company must demonstrate either increased product revenue or entry into a new market to benefit from the deduction.

Robotization Relief

What is Robotization Relief?

An incentive for companies investing in industrial robots and automation. The robotisation tax credit allows companies to deduct an additional 50% of their robotisation-related expenses from their tax base. This tax break is intended to help companies boost their productivity and competitiveness in both domestic and international markets. Companies that use industrial robots to improve production can apply for it.

Key Benefits for Businesses:

- 50% tax deduction of costs related to:

-

- purchasing industrial robots,

- integrating automation equipment,

- implementing related software,

- training employees.

Who is eligible?

- All businesses investing in robotic and automated production systems.

Conditions for Robotization Relief:

- The investment must involve industrial robots as defined by law,

- Unused deductions can be carried forward for up to 6 years if the company is not yet profitable.

Prototype Relief & Tax Incentives in Poland

What is Prototype Relief?

This relief supports the trial production and market launch of new products developed through the company’s R&D activities. The prototype relief allows for an additional deduction of 30% of the deductible expenses for the trial production and marketing of a new product from the tax base. This will enable you to produce a prototype more cheaply and then begin mass production of your invention.

The prototype tax credit will support you during the testing phase of your invention, before you start mass production and launch it on the market.

Key Benefits for Businesses:

- Up to 30% tax deduction of costs related to:

- trial production (prototypes),

- starting the sales process for a new product.

Who is eligible?

- Companies that have developed an original product through internal R&D and want to bring it to market.

Conditions:

- The product must be the result of prior R&D,

- Eligible expenses include those related to trial production or preparing the product for commercial launch.

Withholding tax preferences

Number of double tax treaties concluded by Poland

One significant advantage of investing in Poland is the country’s extensive network of double taxation treaties. Poland has concluded agreements with over 90 countries, including Saudi Arabia, effectively eliminating or significantly reducing the risk of double taxation. These treaties create a favorable tax environment, promoting transparent and efficient cross-border investments.

For investors from the Middle East, especially from Saudi Arabia, this means greater certainty, lower tax burdens, and increased profitability when doing business in Poland.

The Parent–Subsidiary Directive

The Parent–Subsidiary Directive (2011/96/EU) aims to eliminate double taxation on cross-border dividend payments between associated companies within the EU. Poland has implemented this directive into its Corporate Income Tax Act (CIT Act).

Key Benefits in Poland

- Withholding tax (WHT) exemption on dividends paid by a Polish company to an EU/EEA parent company.

- Facilitates tax-efficient repatriation of profits within corporate groups operating across the EU.

Who is eligible?

- Companies that are tax residents of the EU or EEA,

- Holding at least 10% of shares in the Polish distributing company,

- Holding period: at least 2 years (can be ongoing or future commitment).

Conditions:

- Specific documentation requirements (e.g. valid tax residency certificate of the parent company),

- The Polish dividend-paying company must exercise due diligence when applying the exemption.

The Interest & Royalty Directive

The Interest-Royalty Directive (2003/49/EC) seeks to ensure that interest and royalty payments made between related parties in different Member States receive treatment equivalent to comparable domestic transactions. Its primary goal is to eliminate double taxation by prohibiting the imposition of withholding taxes on these payments.

Key Benefit in Poland

- 0% withholding tax on interest and royalty payments made by a Polish company to an associated company in another EU member state (or EEA), provided statutory conditions are met.

Who is eligible?

- Companies of payer and payee must be associated – i.e., one directly holds at least 25% of shares in the other, or both are held by a common parent company (≥25% share),

- The shareholding must be maintained continuously for at least 2 years (can be prospective).

Conditions in Polish Law

- Applies only to qualifying interest and royalty payments (not all fees or services qualify).

- Due diligence obligation – the Polish company must verify the status of the foreign payee and exercise due care,

- Beneficial ownership test – the foreign recipient must conduct genuine economic activity,

- Specific documentation requirements (e.g. valid tax residency certificate of the payee company).

Young Workers & Tax Incentives in Poland

What is it?

This tax relief exempts young individuals from paying personal income tax (PIT) on employment-related income up to a set annual limit. It aims to support the professional activity and financial independence of people under the age of 26.

Key Benefits

- No PIT (income tax) on eligible income up to PLN 85,528 per year (limit for 2025),

- Higher take-home pay for young employees at no additional cost to employers,

- The relief can be applied automatically if the employee submits a declaration to the employer.

Who is eligible?

- Individuals under 26 years of age,

- Earning income from the following sources:

- Employment contracts (umowa o pracę),

- Contract of mandate (umowa zlecenia),

- Student internships or apprenticeship agreements,

- Military service income (since 2023).

Conditions

- The person must be under 26 at the time of earning the income,

- The tax exemption applies only up to the annual income threshold – any amount above this is taxed normally,

- To benefit from the relief during the year, the employee must submit a written declaration to their employer,

- The relief does not apply to business income or contracts for specific work (umowa o dzieło).

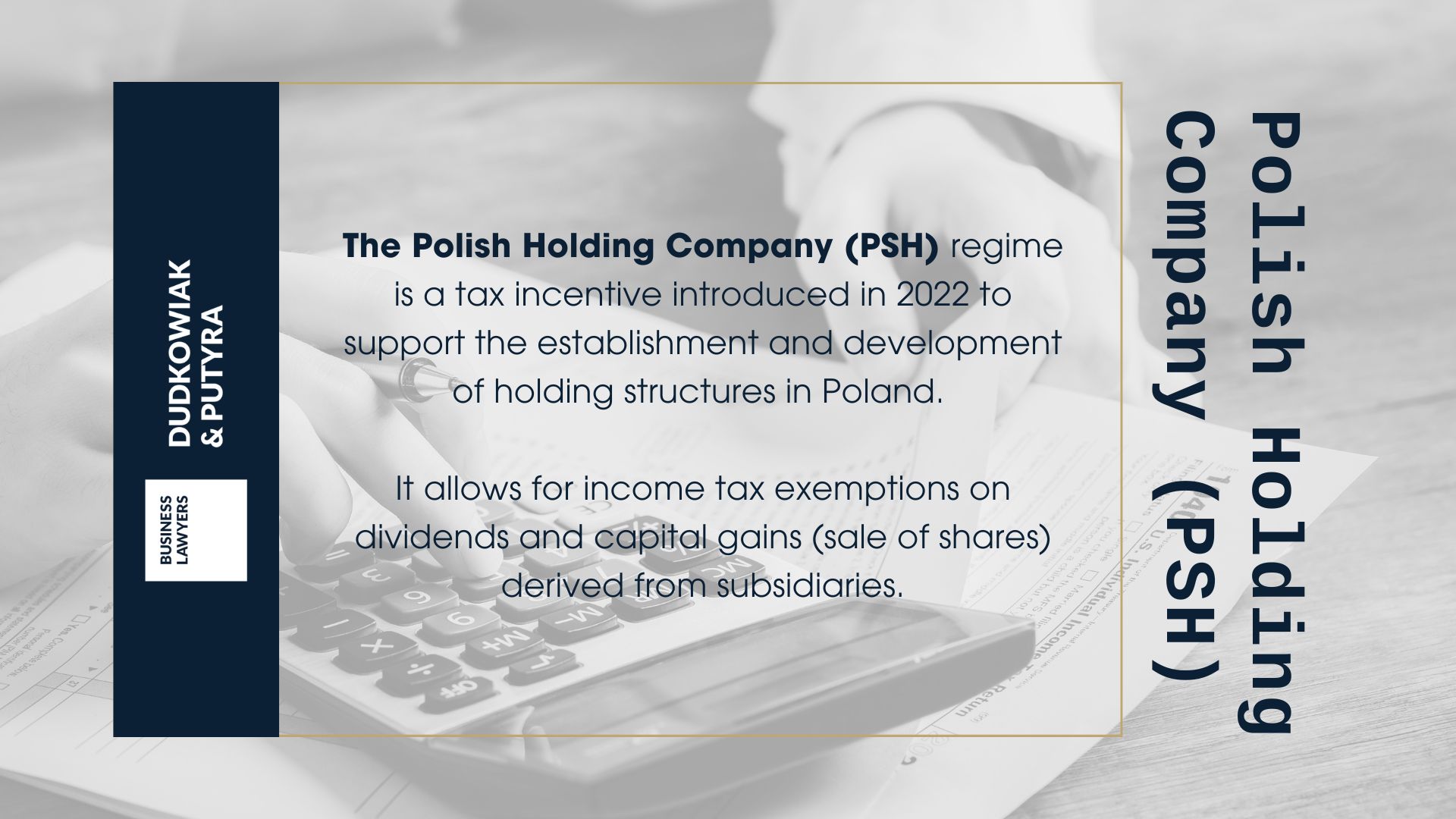

Polish Holding Company (PSH)

What is it Polish Holding Company (PSH)?

The Polish Holding Company (PSH) regime is a tax incentive introduced in 2022 to support the establishment and development of holding structures in Poland. It allows for income tax exemptions on dividends and capital gains (sale of shares) derived from subsidiaries.

Key Benefits

- 100% CIT exemption on dividends received by the Polish holding company from its subsidiaries,

- CIT exemption on capital gains from the sale of shares in subsidiaries (subject to conditions),

- Enables companies to build efficient holding structures in Poland instead of using foreign jurisdictions (e.g. Netherlands, Luxembourg).

Who is eligible?

- A holding company: a Polish limited liability company (sp. z o.o.) or joint-stock company (S.A. or PSA) holding at least 10% of shares in a subsidiary for at least two years,

- A subsidiary: a domestic or foreign capital company whose shares are held by the holding company,

- Both domestic and international investors looking to centralize group management in Poland.

Conditions for the holding company:

- Must be tax resident in Poland,

- May not benefit from special economic zone (SEZ) or Polish Investment Zone (PSI) exemptions,

- Must hold at least 10% of shares in the subsidiary continuously for at least 2 years,

- Must conduct genuine business activity and does not enjoy,

- Its shareholders must not be a tax residents in a blacklisted (non-cooperative) jurisdiction.

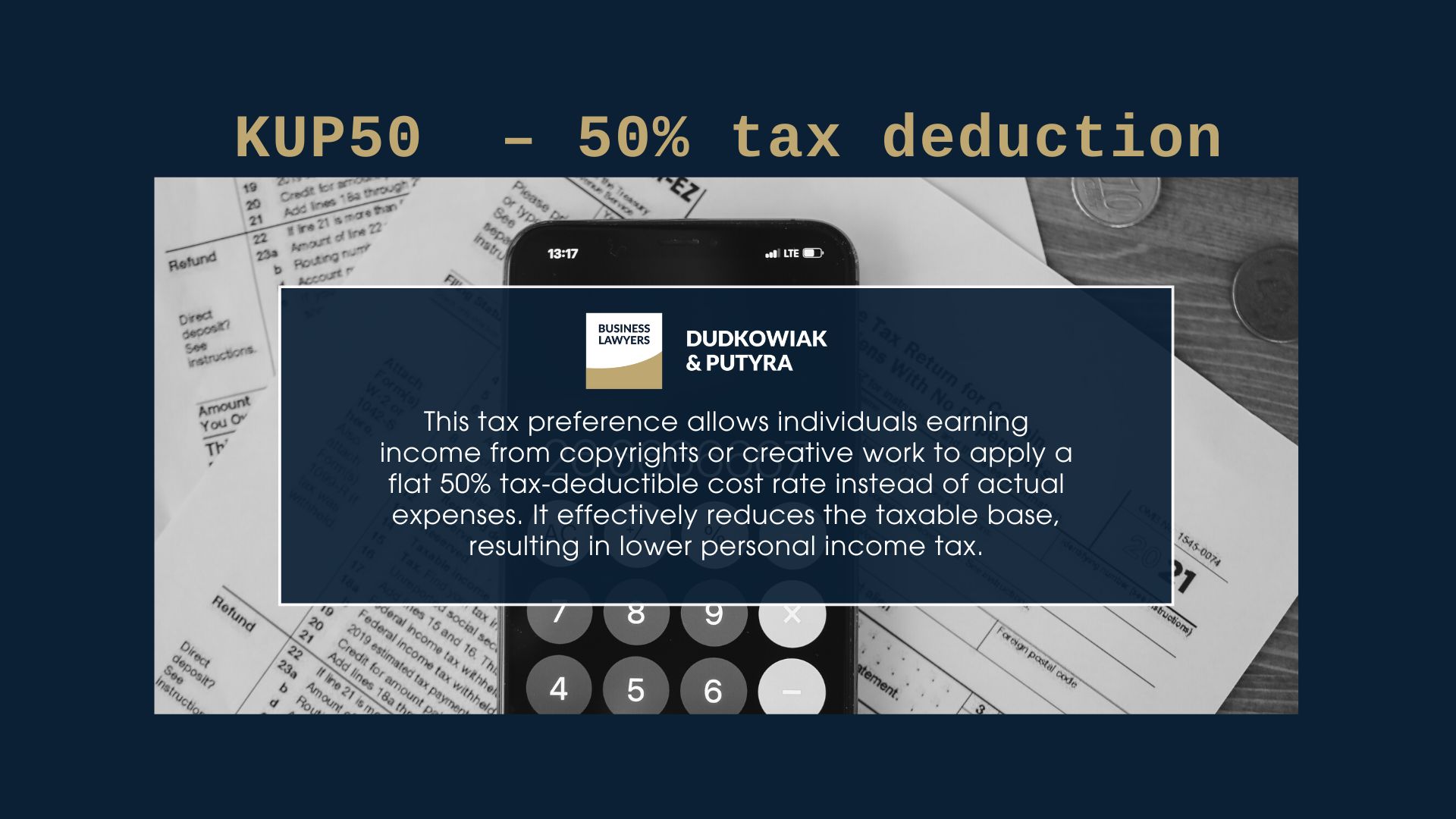

KUP50 – 50% tax deduction

This tax preference allows individuals earning income from copyrights or creative work to apply a flat 50% tax-deductible cost rate instead of actual expenses. It effectively reduces the taxable base, resulting in lower personal income tax.

Key Benefits

- Only 50% of gross income is taxed, meaning significantly lower PIT,

- Applies regardless of actual expenses – no need to document costs,

- Can be used with employment contracts, contracts of mandate, or specific-task contracts (umowa o dzieło),

- Simple mechanism for both taxpayers and employers.

Who is eligible?

- Individuals earning income from copyrighted or creative work, such as:

- Software developers (creating original code),

- Graphic designers, illustrators, architects,

- Writers, journalists, translators,

- Musicians, screenwriters, filmmakers,

- Scientists publishing original research.

Conditions

- The work must be original, creative, and protected under copyright law,

- The income must result from the use or assignment of copyright,

- The copyright component of remuneration must be clearly separated (e.g. in the contract or payslip),

- The annual cap for 50% tax-deductible costs is PLN 120,000 (in costs), which equals PLN 240,000 gross income,

- Not available for income from business activity or management board contracts.

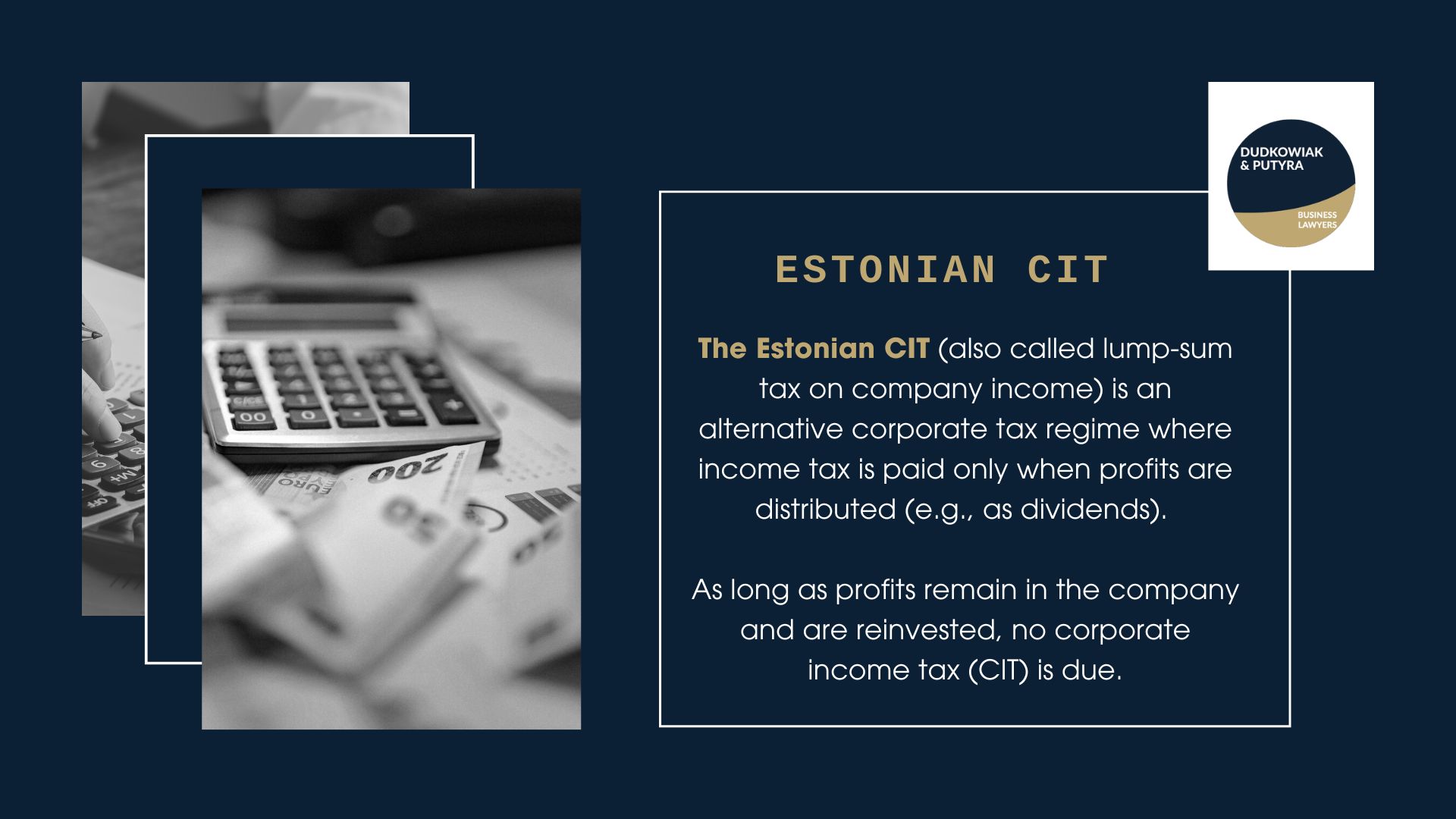

Estonian CIT

What is Estonian CIT ?

The Estonian CIT (also called lump-sum tax on company income) is an alternative corporate tax regime where income tax is paid only when profits are distributed (e.g., as dividends). As long as profits remain in the company and are reinvested, no corporate income tax (CIT) is due.

Key Benefits

- No CIT on retained earnings – full reinvestment is tax-free,

- Simplified tax reporting – no need to calculate taxable income under standard rules,

- Lower effective taxation upon profit distribution:

- 20% CIT + 10% PIT for small taxpayers,

- 25% CIT + 5% PIT for other companies,

- (Effective tax rates after credit: approx. 26.29% and 34.39%)

Who is eligible?

- Limited liability companies (sp. z o.o.) and joint-stock companies (S.A.) based in Poland,

- Owned exclusively by individuals (natural persons),

- Do not hold shares in other entities (no subsidiaries or partnerships),

- Employ at least 3 full-time employees, or meet alternative payroll cost thresholds.

Conditions

- Tax is deferred until profit distribution (e.g., dividends or hidden profits),

- Entry into the regime is voluntary, by filing a formal notification (ZAW-RD),

- Company must maintain full accounting books,

- Certain tax reliefs (e.g., R&D or IP Box) are not available during the Estonian CIT period.

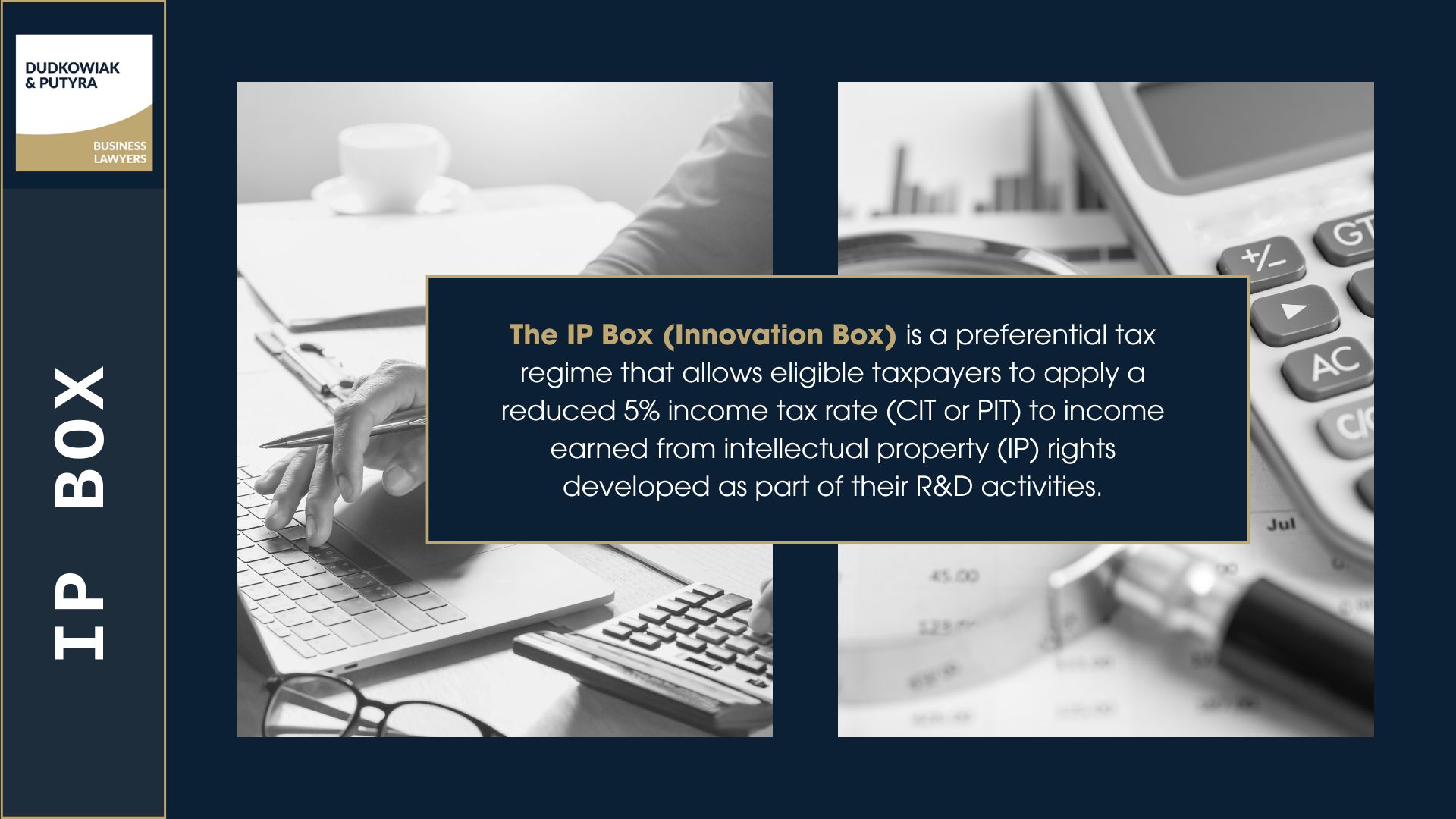

Tax Incentives in Poland Through IP Box

What is IP Box?

The IP Box (Innovation Box) is a preferential tax regime that allows eligible taxpayers to apply a reduced 5% income tax rate (CIT or PIT) to income earned from intellectual property (IP) rights developed as part of their R&D activities.

Key Benefits

- 5% tax rate instead of the standard 12% or 19% (depending on taxpayer type),

- Can be combined with the R&D tax relief, significantly lowering the effective tax burden,

- Encourages innovation by rewarding the commercialization of proprietary technologies and solutions.

Who is eligible?

- Entrepreneurs (individuals or companies) conducting R&D activities,

- Taxpayers generating income from qualified IP rights, such as:

- copyrighted computer software,

- patents,

- utility models,

- industrial designs,

- supplementary protection certificates for pharmaceuticals or plant protection products.

Conditions

- The IP must be created, developed, or improved by the taxpayer as part of their own R&D activity,

- Taxpayer must maintain detailed accounting records to clearly separate income and costs related to the qualified IP,

- Income must result from the use or sale of the IP – e.g., through licensing, royalties, or IP disposal,

- The taxpayer must file an annual tax return with the relevant attachment (CIT/IP or PIT/IP).

FAQ – Tax Incentives in Poland

Why are tax incentives in Poland considered a critical tool for attracting foreign direct investment

Poland’s robust tax incentives framework plays a key role in attracting foreign direct investment by offering a combination of financial incentives, tax exemptions, and credits that support economic growth, job creation, and technological development. These measures help companies and firms improve competitiveness within both local and major economies.

What types of tax benefits are available for companies investing in research, development, or innovation in Poland?

Poland offers various tax benefits, including: tax credits and exemptions, for qualified research expenses, technological innovation, and R&D-related expenditures. Programs such as the R&D relief and IP Box allow eligible businesses to reduce their income tax based on their innovation-driven activities and performance.

How do Special Economic Zones (SEZs) and the Polish Investment Zone (PSI) support economic development?

Special Economic Zones and the Polish Investment Zone were established to enhance trade, promote development, and stimulate investment by offering state aid, tax exemption, and supportive regulations. These economic zones also focus on enhancing the local workforce, especially in areas facing high unemployment, and encourage employers to invest in new or existing business components.

Who is eligible to claim tax reliefs such as the R&D credit, robotization relief, and prototype relief?

Eligibility is generally based on meeting criteria such as incurring qualified expenditures, passing a business component test, and aligning with certain regulations. These reliefs are accessible to a broad range of companies, including large multinational corporations and local firms, provided they conduct research, innovation, or development within Poland’s regulatory environment.

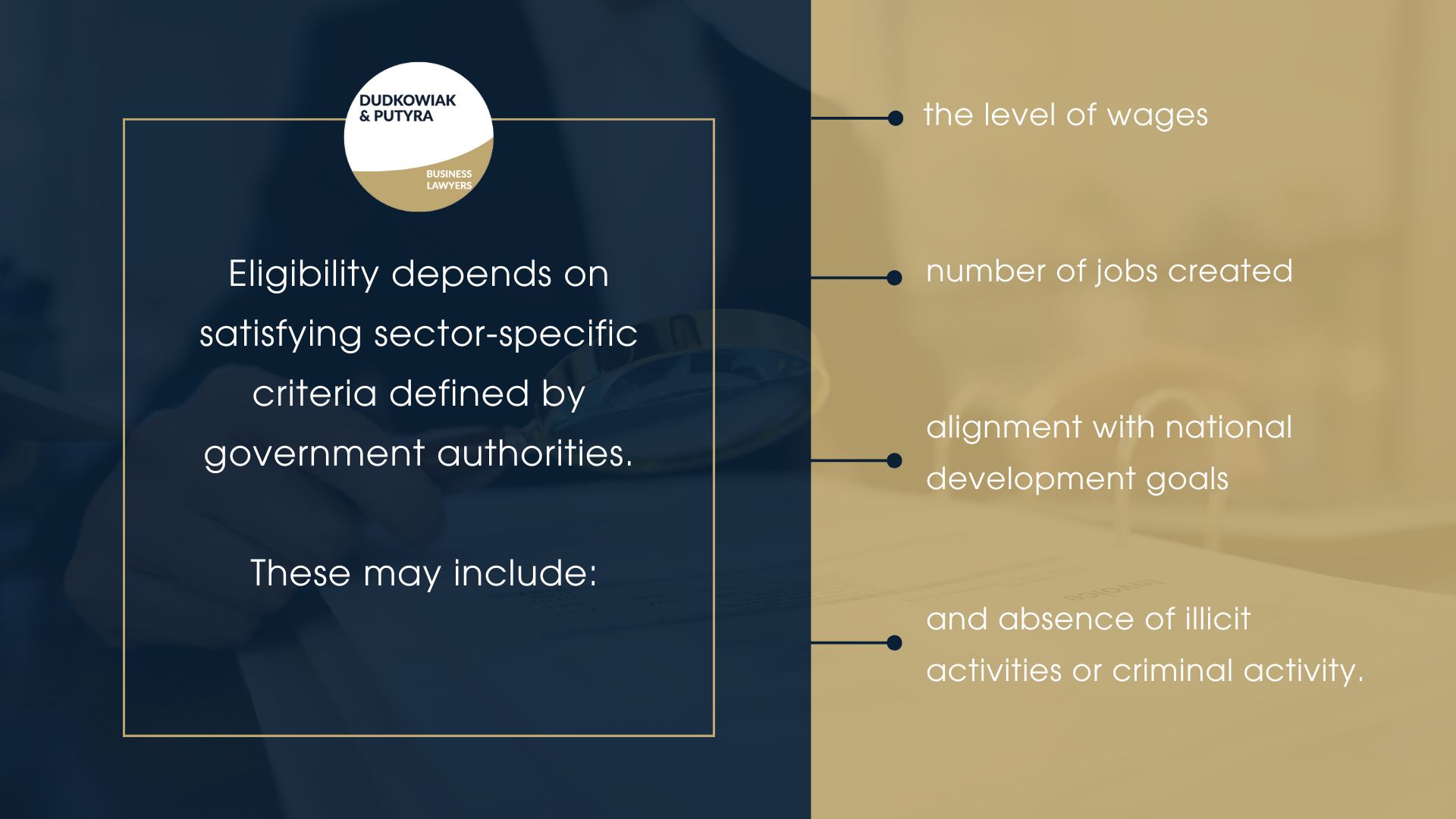

What conditions determine a company’s eligibility for tax incentives in Poland?

Eligibility depends on satisfying sector-specific criteria defined by government authorities. These may include the level of wages, number of jobs created, alignment with national development goals, and absence of illicit activities or criminal activity.

Can tax incentives in Poland be carried forward if a company is not yet profitable?

Yes, many tax credits – such as those related to R&D, robotization, or expansion – can be carried over into future tax years, especially within the first five years after becoming eligible. This allows businesses to plan long-term, maximize tax benefits, and gradually improve their financial performance without losing access to critical incentives.