New Obligations from June 2025 – Do Your Financial Services Meet Accessibility Requirements?

On 28 June 2025, the Act of 26 April 2024 on Ensuring that Business Entities Meet Accessibility Requirements for Certain Products and Services (Journal of Laws 2024, item 731), implementing the so-called European Accessibility Act (EAA), will enter into force.

Although this act is primarily associated with the obligations of electronic equipment manufacturers, its provisions also apply to payment service providers and digital service providers, including CASPs (VASPs).

Who is affected by the Act?

The personal scope of the Act includes, among others, national payment institutions (NMIs), small payment institutions (MIPs), as well as digital service providers operating as CASPs (Crypto-Asset Service Provider). All of these entities, if they offer e-banking, payment terminals, mobile applications or online payment and financial services, among others, will have to ensure their accessibility for persons with disabilities.

What does ‘accessibility’ mean?

Accessibility is understood as the property of a product or service to enable it to be used for its intended purpose by persons with special needs on an equal basis with other users, which is achieved through the use of universal design or, where this is not possible, through the use of reasonable accommodation as referred to in Article 2 of the Convention on the Rights of Persons with Disabilities, drawn up in New York on 13 December 2006. (OJ 2012, item 1169 and 2018, item 1217); it is regulated, inter alia, in European standards (e.g. EN 301 549).

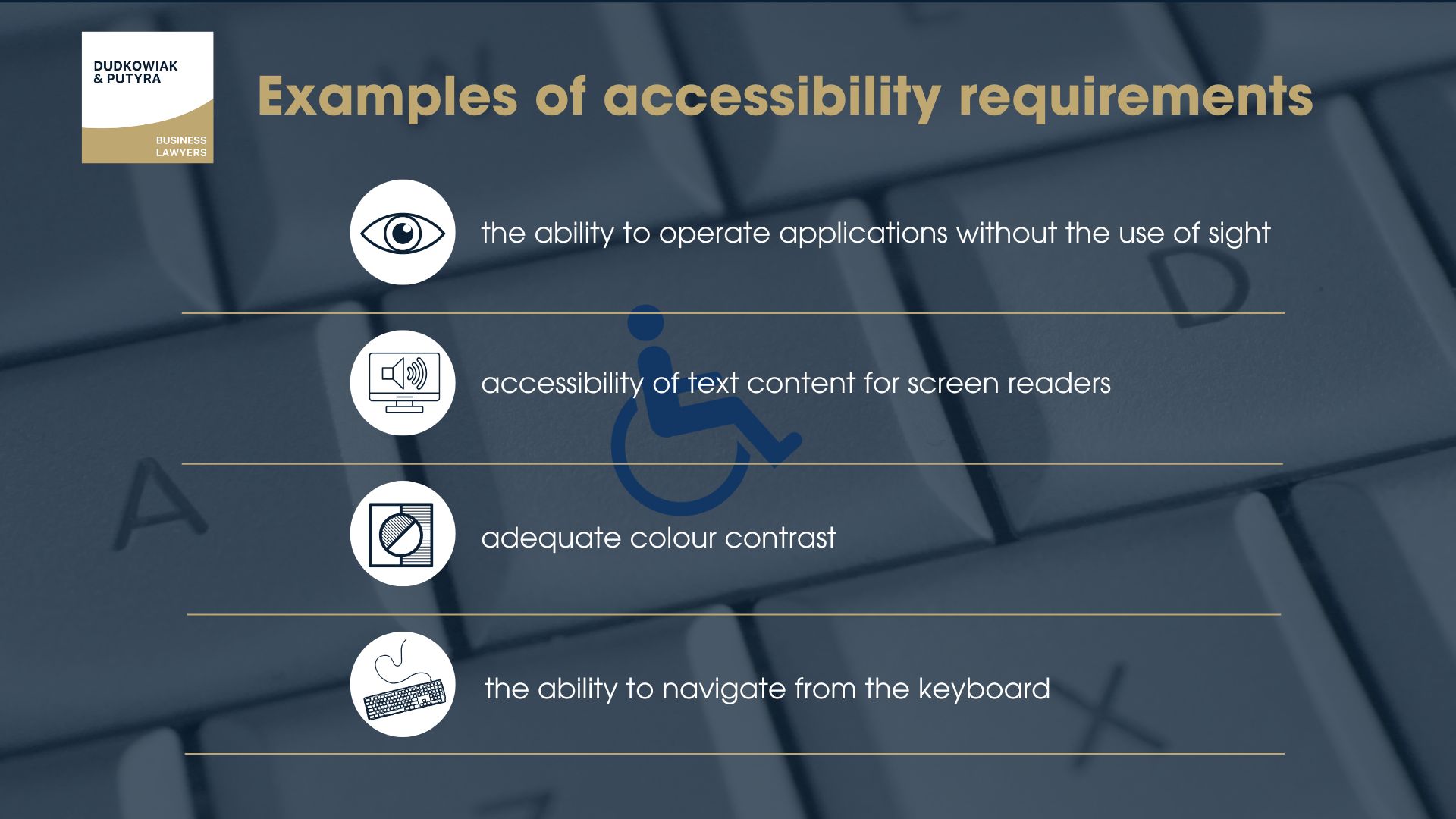

Examples of accessibility requirements include:

- the ability to operate applications without the use of sight,

- accessibility of text content for screen readers,

- adequate colour contrast,

- or the ability to navigate from the keyboard.

Responsibilities of MIP, KIP and CASP

These entities will be required to:

- design and implementation of services with ‘design for all’ principles in mind,

- ensure the availability of customer communication channels (e.g. hotline, correspondence, onboarding processes),

- keeping records to prove that services comply with accessibility requirements,

- the application of corrective procedures when non-compliance is identified.

It is worth emphasising that the obligations apply not only to new services, but – in certain cases – also to significant modifications of existing systems.

Exceptions and concessions

The law provides exceptions for micro-entrepreneurs (up to 10 employees and a turnover of up to €2 million).

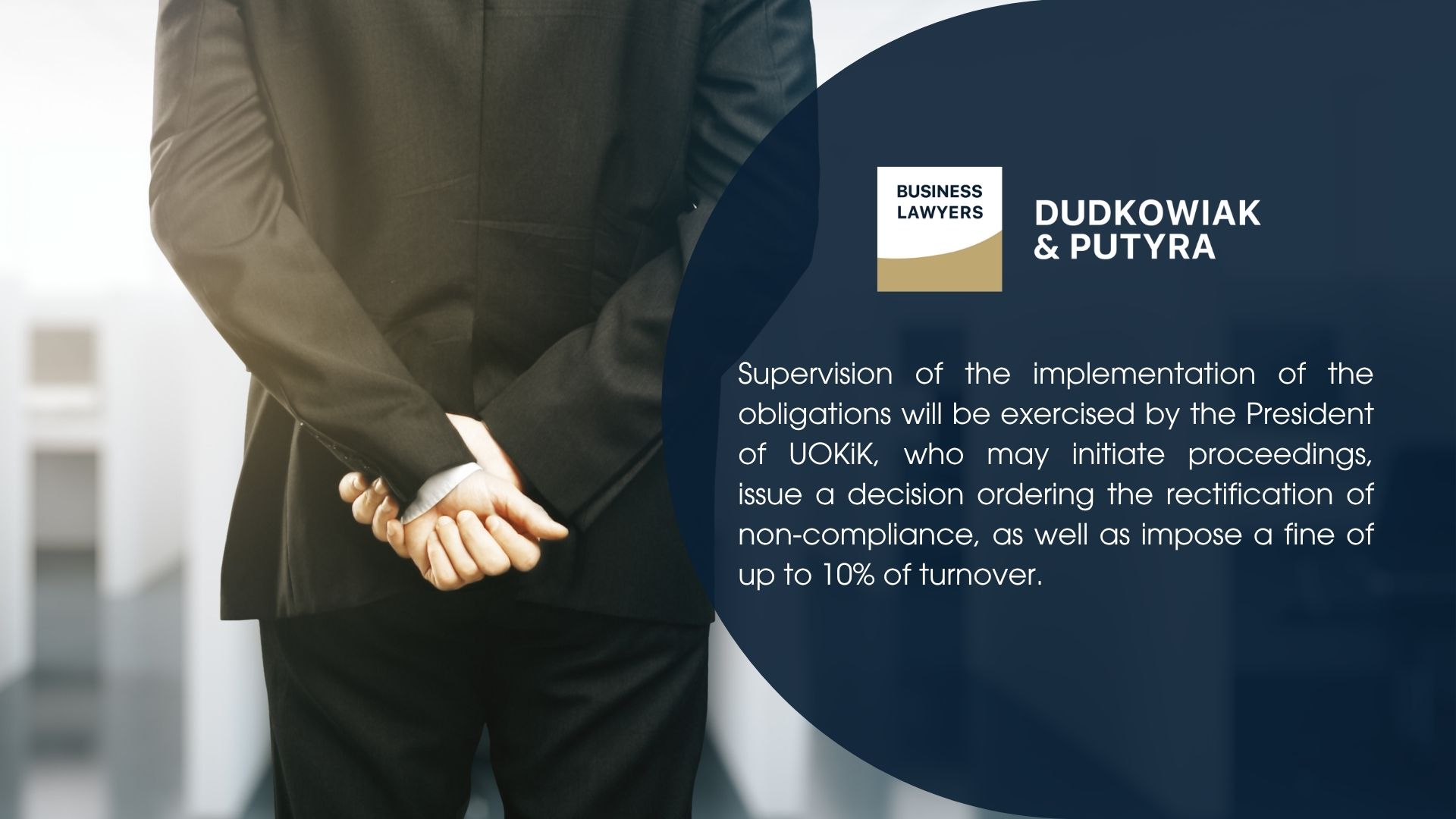

Sanctions and enforcement

Supervision of the implementation of the obligations will be exercised by the President of UOKiK, who may initiate proceedings, issue a decision ordering the rectification of non-compliance, as well as impose a fine of up to 10% of turnover.

Rising Customer Expectations and Regulatory Risk – Why You Should Act Now

In practice, MIPs, KIPs and CASPs should start today to audit the accessibility of their digital services and plan corrective actions. Failure to act could expose the entity to the risk of sanctions and reputational damage – especially in the context of increasing customer expectations for equal access to services.

If your payment institution or CASP offers digital services, it is worth checking today whether they meet the new accessibility requirements. Contact our experts to conduct a compliance audit and develop an action plan to adapt – before the regulations come into force.

And if you want to stay up to date with further regulatory changes, we encourage you to subscribe to our newsletter. Every month, we will send you the most important changes in law and practical information for the Fintech sector.