Draft Tax Law Changes Expand Personal Liability for Those Running Companies

The draft amendments to the Tax Ordinance, prepared in response to the CJEU rulings in Adjak and Genzyński, may significantly increase the risk of personal liability for companies’ tax arrears. The new rules expand the circle of liable persons and move away from formal bankruptcy-related criteria towards an assessment based on due diligence. In practice, this will result in greater discretion for tax authorities and a real risk of enforcement against the assets of those effectively managing the company.

CJEU Rulings and Their Impact on the Polish Legal System

The CJEU judgments in cases C-277/24 Adjak and C-278/24 Genzyński did not completely overturn the liability of management board members for the company’s tax arrears under Article 116 of the Tax Ordinance. The CJEU confirmed that the Polish model may continue to function, but only if it is interpreted in accordance with EU standards.

In the Adjak judgment, the CJEU held that a board member need not be a party to the assessment proceedings against the company, but must have a genuine right of defense in their own proceedings. In contrast, the Genzyński judgment indicated that a board member’s liability cannot be purely objective in nature, but must remain linked to an assessment of their diligence.

To align the interpretation of Article 116 of the Tax Ordinance with the CJEU judgments, the Minister of Finance and Economy issued General Tax Ruling No. DTS2.8012.5.2025, in which he indicated that these judgments necessitate a pro-EU interpretation of Article 116 of the Tax Ordinance and a revision of the existing practice regarding its application.

Recently, however, the Ministry of Finance has taken another step toward adjusting the rules governing third-party liability for a corporation’s tax arrears—it published a draft bill amending the provisions of the Tax Ordinance. And although, according to the description of the draft, its primary objective remains the alignment of regulations with EU law as interpreted by the CJEU, a thorough analysis of the draft leaves no doubt—the changes are significantly broader and may lead to a deterioration in the situation of individuals performing management functions in companies.

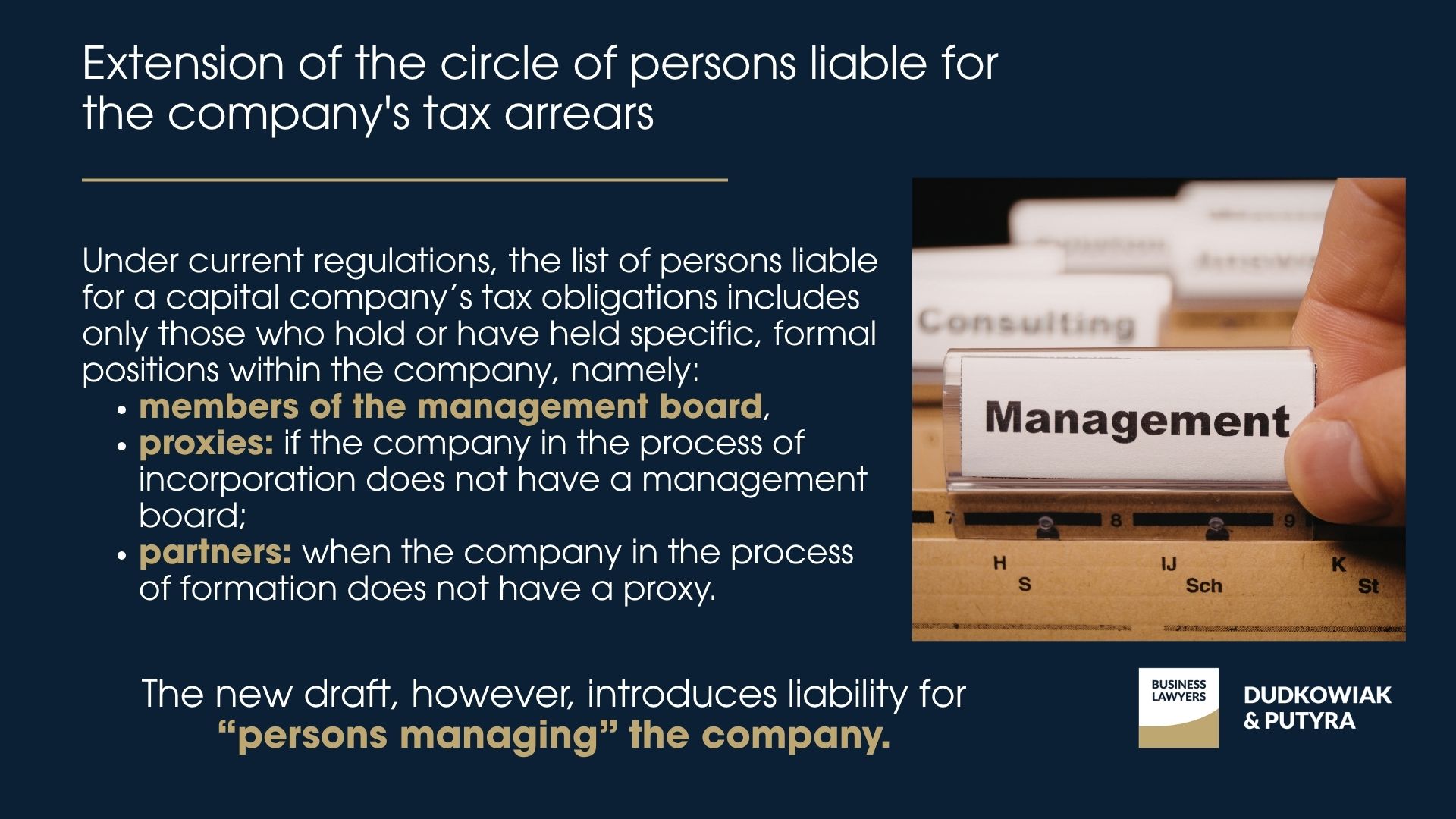

Extension of the circle of persons liable for the company’s tax arrears

The draft amendments to the Tax Ordinance clearly expand the group of persons who may be held liable for a company’s tax arrears under Article 116 of the Tax Ordinance.

Under current regulations, the list of persons liable for a capital company’s tax obligations includes only those who hold or have held specific, formal positions within the company, namely:

- members of the management board,

- proxies: if the company in the process of incorporation does not have a management board;

- partners: when the company in the process of formation does not have a proxy.

The new draft, however, introduces liability for “persons managing” the company.

This category will include all the persons listed above, as well as those who actually, directly or indirectly, exercise management functions within the company.

The draft thus provides for the extension of liability for the company’s tax obligations to include persons whom the tax authorities deem, based on an evaluative (ambiguous) criterion, to be those who actually manage the company.

The explanatory memorandum indicates that this primarily concerns cases of so-called “front men” acting on behalf of the company, the actual performance of functions without proper authorization, or the control of the company through more complex ownership structures.

At the same time, the explanatory memorandum to the draft stipulates that not every proxy or authorized representative will automatically become a liable party—this will only occur if their formal role serves merely as a facade for the actual, independent management of the company’s affairs.

For taxpayers, this means above all that the formal structure of corporate bodies alone will no longer be a sufficient protective shield, and the authorities will gain a stronger basis for holding accountable those who actually make decisions within a given entity.

Liability based on the principle of due diligence

Under the current model, a condition for a board member to be released from personal liability for the company’s tax arrears includes, among other things, filing a petition for the company’s bankruptcy within the prescribed time limit, initiating restructuring, or demonstrating that the failure to file for bankruptcy or restructuring occurred through no fault of the board member.

Following the changes, this model is set to undergo a significant overhaul. The draft legislation moves away from linking liability to bankruptcy law and shifts the burden to assessing whether the person managing the company exercised due diligence in conducting its affairs.

As a result, the tax authority will examine whether each of the persons managing the company acted as a professional who effectively supervises the company and ensures the proper fulfillment of tax obligations.

The draft also assumes that, since tax arrears has arisen, a lack of due diligence can generally be presumed, unless the person in question proves otherwise.

Liability may be avoided not only by demonstrating due diligence but also if the corrective measures taken lead to the payment of most of the arrears or if the arrears arose due to force majeure.

In practice, the introduction of these changes will mean that instead of a dispute over formal grounds for bankruptcy, the proceedings will examine how the company’s affairs were actually managed and whether due diligence worthy of a professional was exercised in the process.

Liability Even After Deletion from the Register, but with the Right to Defense

Current regulations do not explicitly address what happens to liability under Article 116 of the Tax Ordinance when a company is struck from the register or liquidated during proceedings concerning the amount of its tax liability.

The draft aims to clarify this: in such cases, the company’s removal from the register will not block further proceedings, and the authority will be able to resolve assessment issues directly in a decision against a third party. In other words, the company’s removal from the register will no longer close the case.

A positive aspect is that the draft strengthens the procedural position of the person from whom the tax authority seeks to collect arrears. Following the changes, such a person will have a statutory right to access the files of the assessment proceedings conducted against the company and the ability to challenge the factual findings and legal assessments on which the authority bases its decision.

For taxpayers, this means, on the one hand, that authorities will have greater powers once a company is removed from the registry, but on the other hand, it provides stronger safeguards for those held liable for the company’s outstanding obligations.

Is your company prepared for expanded liability for tax arrears?

If the proposed changes may affect your company, it is essential to identify potential risks at an early stage- both for board members and those effectively managing the business. The new liability model, based on due diligence, increases the discretionary powers of tax authorities and requires a more proactive approach to risk management.

We support clients in assessing exposure to liability for companies’ tax arrears, developing risk mitigation strategies, and representing them in proceedings before tax authorities. If you would like to evaluate your position or prepare for the entry into force of the new regulations, please contact our team.